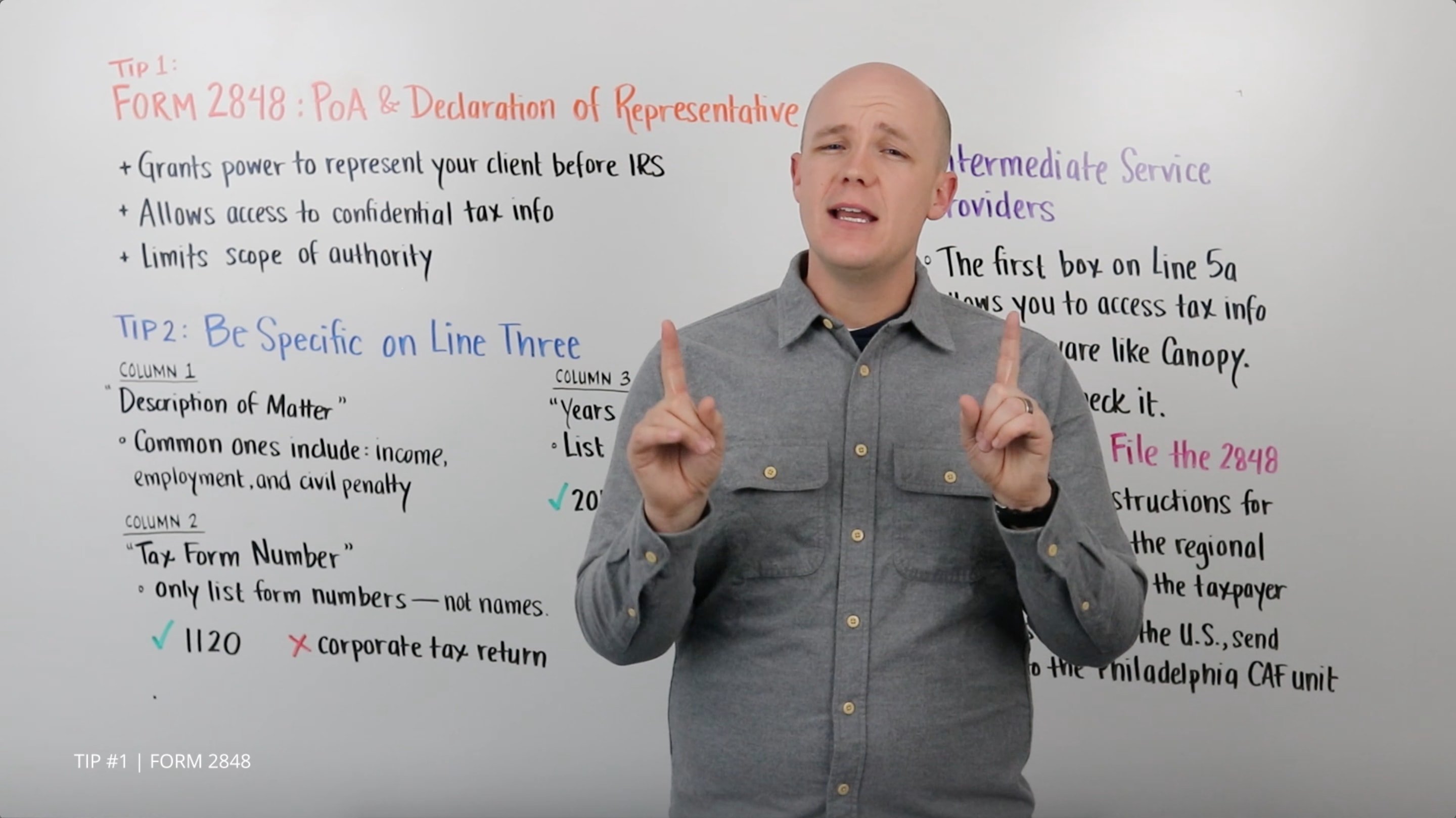

Hi, and welcome to another IRS forms video. Today we’re tackling IRS Form 12277, Application for Withdrawal of Federal Tax Lien. Getting the IRS to withdraw a lien can be a huge benefit for your clients. Let’s take a look at what that takes, and how you can use form 12277 to make it happen.

Try Canopy for free and never manually fill out another IRS form again.

Tip 1: How to Resolve IRS Liens and When to Use Form 12277

When a taxpayer lets their tax debt go unaddressed for too long, the IRS will respond by placing a lien on their assets. By issuing a lien, the IRS is asserting a legal claim to a taxpayer’s property as a security against debt the taxpayer owes to the IRS.

That claim, if left unchecked, will end with the IRS seizing the taxpayer’s assets—bank accounts, valuables, real assets with equity—in an attempt to fulfill the outstanding tax debt.

IRS liens can be resolved in two different ways—release and withdrawal.

A lien release gets rid of most of the immediate effects of a lien. Because the IRS no longer has any interest in the assets, your client may sell or transfer their assets at will.

The IRS will release a lien 30 days after the tax debt has either been satisfied through an installment agreement or Offer in Compromise. A lien will also automatically be released 30 days after the collections statute expiration date, or CSED, or if the tax debt is discharged in bankruptcy.

A lien release, however, does not erase all of the effects of a lien. The lien will remain on the taxpayer’s credit history unless the IRS withdraws the lien. A withdrawn lien can be removed from the client’s credit history as if it had never been issued.

IRS Form 12277 is the form you will use to request that withdrawal.

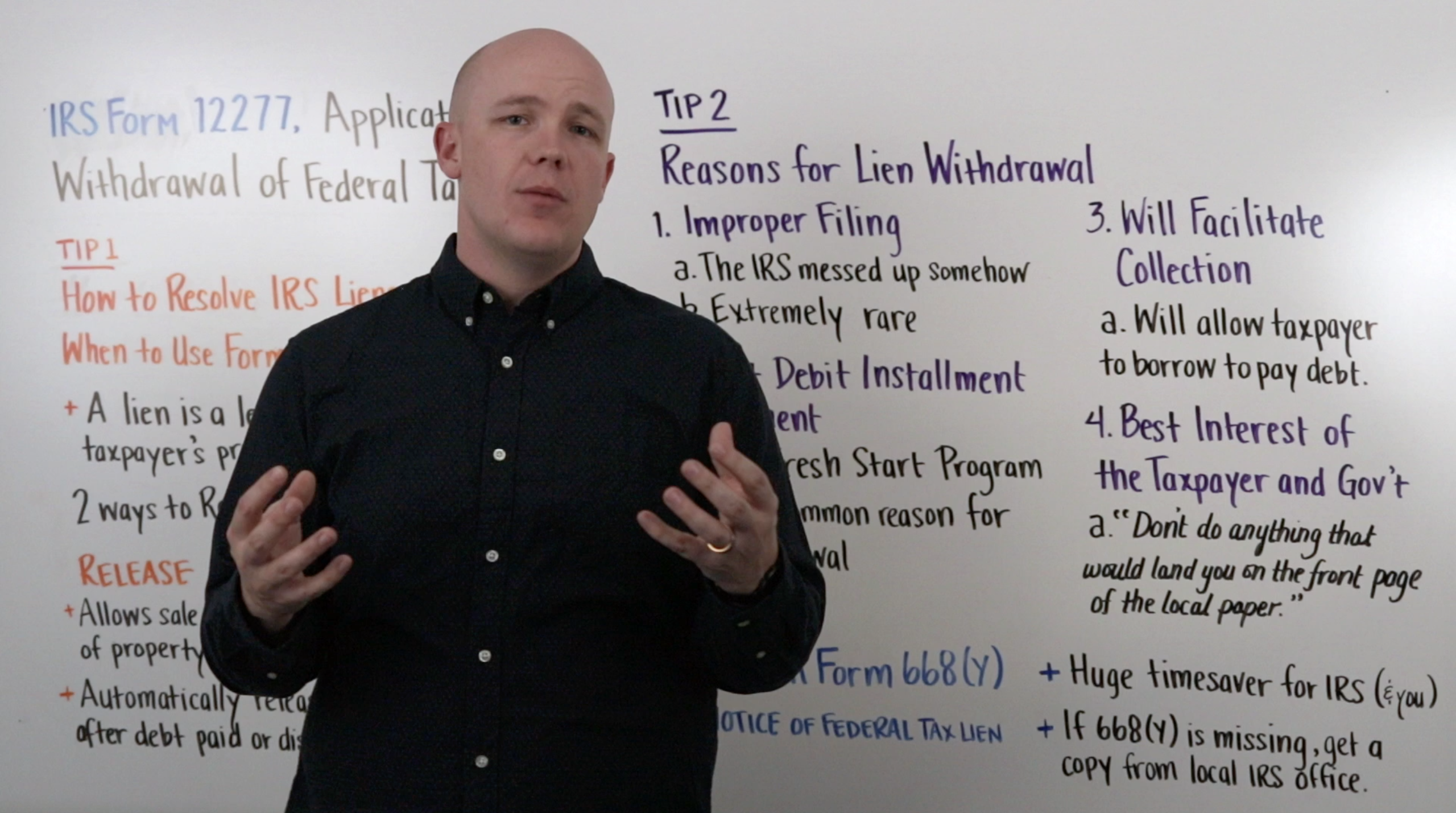

Tip 2: Reasons for Lien Withdrawal

Getting a lien withdrawn is obviously the preferable option, so how do you know if your client qualifies to have their lien withdrawn?

On Form 12277, line 11 lists four reasons they will consider withdrawing the lien.

“The Notice of Federal Tax Lien was filed prematurely or not in accordance with IRS procedures.”

The IRS will withdraw the lien if the tax that eventually prompted the lien was assessed in error, or if the lien was filed without giving the taxpayer proper notice in advance. This is extremely rare, as the IRS has multiple fail-safes in place to avoid these kinds of mistakes. However, mistakes do still happen, and the IRS will withdraw the lien if you can prove it.

“The taxpayer entered into an installment agreement to satisfy the liability for which the lien was imposed and the agreement did not provide for a Notice of Federal Tax Lien to be filed.”

This is the most common method of getting a lien withdrawn. The IRS Fresh Start Program allows the IRS to withdraw a lien if the taxpayer has entered into a Direct Debit Installment Agreement. In order to qualify for withdrawal, the taxpayer must have filed all their required tax returns for the last three years and must be current with any estimated tax payments.

“Withdrawal will facilitate the collection of the tax.”

Because a tax lien is so detrimental to a taxpayer’s credit, it will often affect their ability to borrow money. If the IRS can be convinced that withdrawing a lien will allow the taxpayer to borrow money and pay off their tax debt, they will likely withdraw the lien.

“The taxpayer, or the Taxpayer Advocate acting on behalf of the taxpayer, believes withdrawal is in the best interest of the taxpayer and the government.”

This option is hard to quantify exactly because “best interest” is hard to nail down. But according to a former IRS Revenue Officer who now works at Canopy, the advice commonly given at the IRS was, “Don’t do anything that would land you on the front page of the local paper.”

Basically, the IRS doesn’t want to get caught putting a lien on the house of the 90-year-old widow living on Social Security. If you’ve got a situation you think merits special consideration, check this box on form 12277.

Tip Three: Attach Form 668(Y), Notice of Federal Tax Lien

Line nine of form 12277 instructs you to “Attach copy of the Form 668(Y), Notice of Federal Tax Lien, if available,” or provide information about the notice. Attaching a copy of the actual notice will be a huge time saver for the IRS, and therefore for you and your client. Even if your client doesn’t have a copy of the lien, you can often get a copy from your local IRS office without too much hassle.

Well, that’s all we have for you today. Be sure to check out our other videos for all your IRS form filling needs. Also, please like the video and subscribe to be notified when we put more helpful videos. If you have any questions or suggestions for other forms we should cover, let us know in the comments.

Get Our Latest Updates and News by Subscribing.

Join our email list for offers, and industry leading articles and content.