We've put together another video to help you when you're representing a client. In this video, we cover some tips on how to fill out IRS Form 2848 to make sure your request for power of attorney gets approved the first time. Watch it below and subscribe to our Youtube channel to be notified when we put out other helpful videos.

Get IRS Form 2828 here

Video Transcript:

Hello and welcome!

In this video, we’re going to talk about IRS Form 2848: Power of Attorney and Declaration of Representative.

We will explain what this form authorizes, who should use it, plus some helpful tips to make sure that the IRS will approve your request for Power of Attorney.

Let’s jump in.

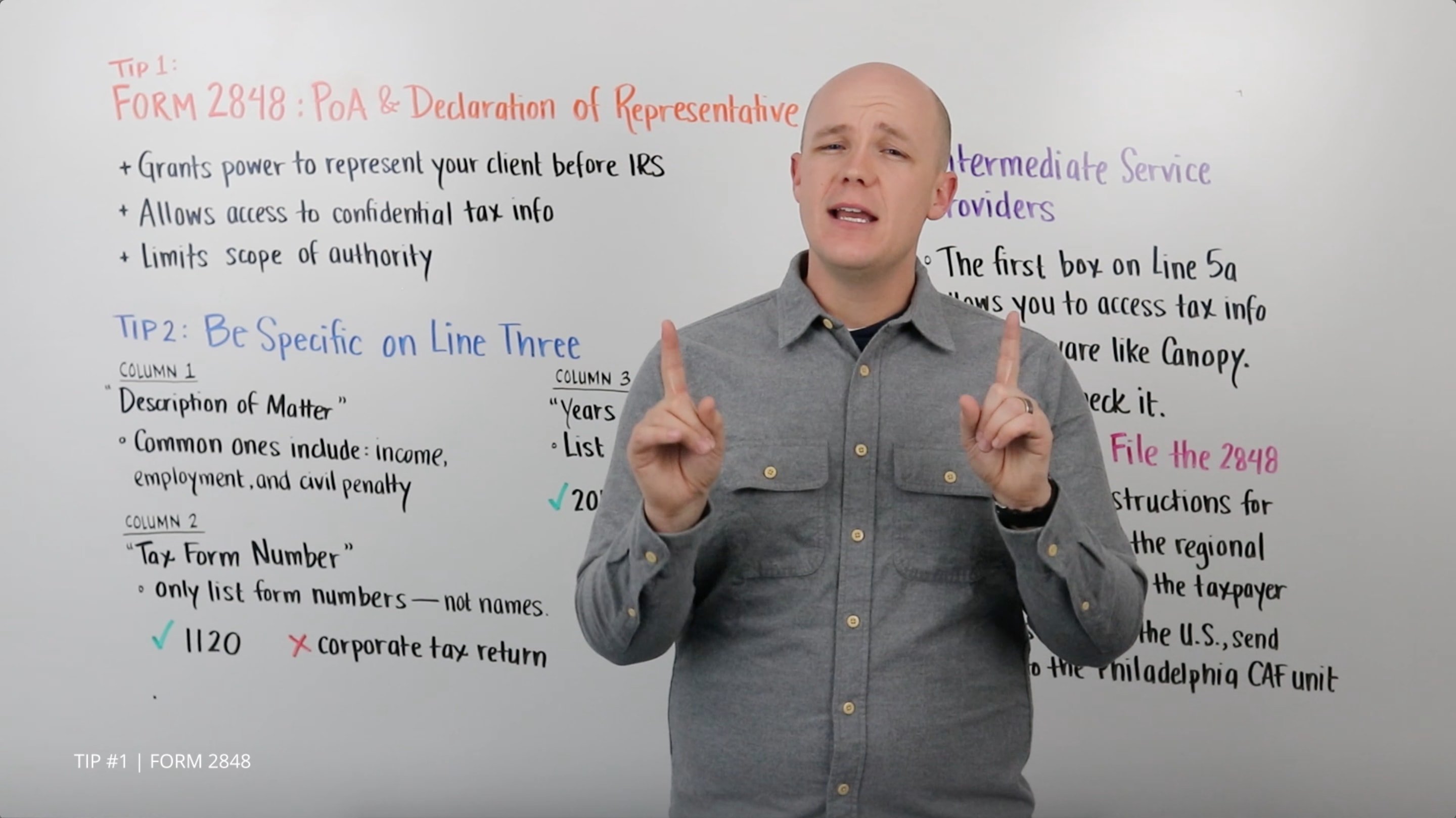

Tip 1: What is IRS form 2848 and who should use it?

Only certain people can be granted Power of Attorney using form 2848. For tax professionals that group includes attorneys, CPAs, and enrolled agents. The form allows these tax professionals to represent their client before the IRS as if they were the taxpayer.

There are a number of reasons this type of representation may be necessary. Maybe your client is out of the country during tax season or they are limited in their ability to communicate because of a medical condition. Maybe you represent a corporation or individual with unresolved tax debt. The 2848 allows you to define and limit the scope of the authority your client wishes to grant. More on that in a moment.

A successfully filed 2848 also gives a tax professional the authority to receive confidential tax information for their client, including tax returns, transcripts, and IRS notices. However, if you’re only looking for access to your client’s tax documents, you may be better off using the much simpler form 8821.

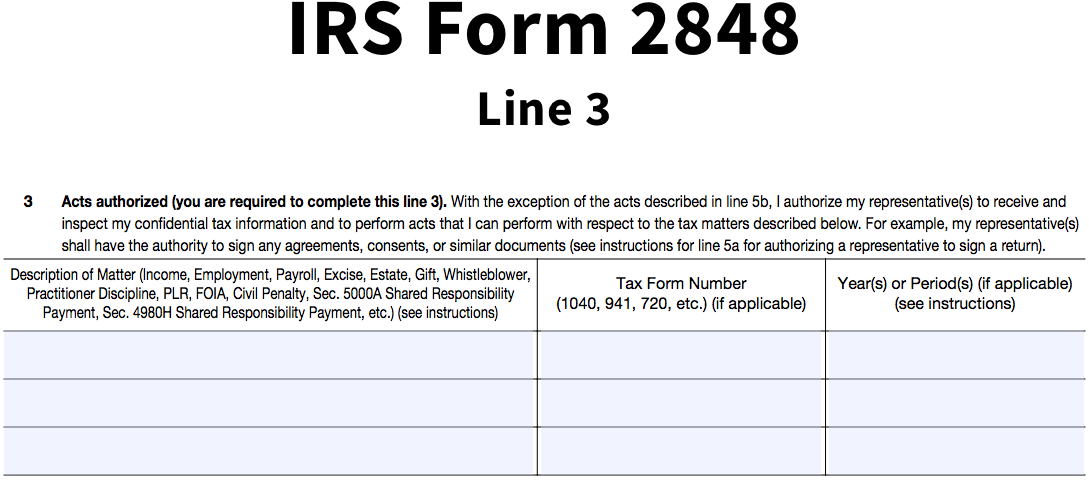

Tip 2: Be Specific on Line Three

The 2848 gets rejected a lot and it’s usually because people don’t follow the instructions when filling out line three. While filling out this section, you must clearly state the specific issue or issues that you are requesting authorization for. This includes the nature of the issue, the types of forms involved, and the specific period of time that this authority will be granted.

In line three you must be specific. Using general terms like “all taxes” or “all years” in this section will result in a rejected POA request.

Let’s go through line three column by column so that this doesn’t happen to you.

Column 1

This is where you describe the type of tax or issue you’ll be dealing with. Common descriptors in this column can include income, employment, civil penalty, and circular 230 violation. If you’re representing a client in regards to a penalty or other collections issue, you would list the type of tax associated with the issue. For instance, if you are assisting an individual who owes back taxes to the IRS you would list “income” in column one.

Column 2

For the second column, you will list the forms that you need access to. When filling it out, it’s extremely important to specifically list the form numbers. Lots of people write the title of a form instead of the form number, resulting in a denied request. For instance, if you’re representing a corporation and need access to their corporate tax return, write form 1120 in column two, not “corporate tax return.” If you need access to multiple forms, make sure to list them all in the rows provided.

Column 3

This column identifies the specific periods for which you are authorized to access forms. You can specify calendar years, quarterly periods, or even intermittent time periods. If you want to have the authority to pull forms from 2014 to 2016, simply write “2014 thru 2016” in the third column.

Tip 3: Intermediate Service Providers

Another section worth paying attention to is line five - specifically the new checkbox on line 5a. There are multiple boxes you can check, but we’re going to focus on the one dealing with accessing IRS documents from an intermediate service provider.

By checking this box, tax information (such as transcripts) can be easily accessed through third party software like Canopy. If this box is left unchecked, you can only obtain tax information the old-fashioned way—directly from the IRS.

If you’re not sure whether or not to check this box - check it! Checking this box gives you multiple options for retrieving your client’s tax documents.

Tip 4: Where to file the 2848

So you’ve finished filling out form 2848 with all of the correct information. Now where does it go?

This form almost always gets sent to the regional CAF unit associated with the state where the Taxpayer resides. Unless you’re dealing with the IRS directly and they specifically request the form, you will mail this document to the client’s regional CAF unit—either Ogden, Utah or Memphis, TN—based on your client’s home address. If the Taxpayer lives outside the US, you should send the 2848 to the CAF unit in Philadelphia. To find the address of the CAF unit assigned to your Taxpayer’s state, check the link in our video description.

Let’s recap:

IRS form 2848 is designed to give attorneys, CPA’s, and enrolled agents authority to receive confidential tax documents and represent their client before the IRS.

Be specific when filling out line 3. Clearly state the issue, forms, and time periods to avoid getting your power of attorney request denied General information is not your friend here.

Determine where your tax documents will be retrieved from. If an intermediate service provider will be used, check that first box in line 5a.

Make sure to check the instructions for form 2848 to see which CAF unit you should send your finished form. The link to the instructions is in the description.

And that’s all we have for you on IRS form 2848! Thanks for watching.

Comment below if you have any tips for the 2848 that we didn’t get to. Also, feel free to comment if you have any suggestions for videos you would like to see in the future.

See you next time!

Canopy is a one-stop-shop for all of your accounting firm's needs. Sign up free today to see how our full suite of services can help you.

Get Our Latest Updates and News by Subscribing.

Join our email list for offers, and industry leading articles and content.